Understanding and Managing Accrued Curiosity within the Chart of Accounts

Associated Articles: Understanding and Managing Accrued Curiosity within the Chart of Accounts

Introduction

With enthusiasm, let’s navigate by the intriguing subject associated to Understanding and Managing Accrued Curiosity within the Chart of Accounts. Let’s weave fascinating info and supply recent views to the readers.

Desk of Content material

Understanding and Managing Accrued Curiosity within the Chart of Accounts

Accrued curiosity, a crucial element of economic reporting, represents curiosity earned or owed however not but acquired or paid. Correctly dealing with accrued curiosity inside your chart of accounts is essential for correct monetary statements, well timed tax filings, and sound monetary decision-making. This text delves into the intricacies of accrued curiosity, its accounting therapy, widespread chart of account classifications, potential pitfalls, and finest practices for efficient administration.

What’s Accrued Curiosity?

Accrued curiosity arises from the passage of time on interest-bearing devices. It is the curiosity that has been earned or incurred however stays unpaid on the reporting interval’s finish. This contrasts with acquired curiosity, which displays funds truly collected or made. The accrual accounting precept mandates recognizing income and bills when they’re earned or incurred, no matter when money modifications fingers. Because of this accrued curiosity is a vital adjustment in monetary reporting.

Examples of Accrued Curiosity:

-

Accrued Curiosity Receivable: This arises when an organization lends cash (e.g., by notes receivable) or invests in interest-bearing securities (e.g., bonds). The curiosity earned in the course of the interval however not but acquired is recorded as an asset (Accrued Curiosity Receivable).

-

Accrued Curiosity Payable: This arises when an organization borrows cash (e.g., by financial institution loans or bonds payable). The curiosity expense incurred in the course of the interval however not but paid is recorded as a legal responsibility (Accrued Curiosity Payable).

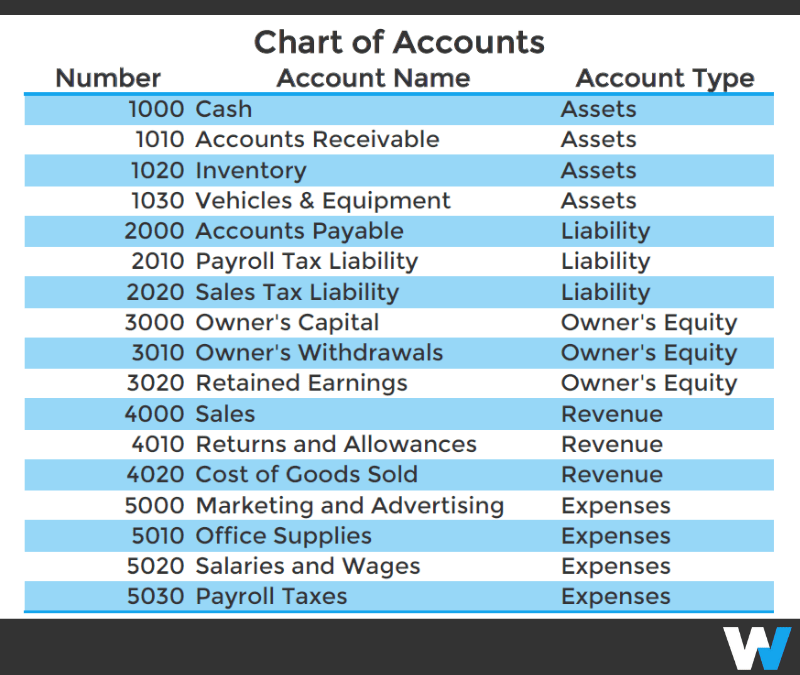

Chart of Accounts Classification:

The precise account titles used to signify accrued curiosity range relying on the corporate’s chart of accounts construction and accounting software program. Nonetheless, widespread classifications embody:

-

Accrued Curiosity Receivable: This account is usually discovered throughout the present property part of the stability sheet. Sub-accounts could also be used to additional categorize the supply of the receivable (e.g., "Accrued Curiosity Receivable – Buyer Loans," "Accrued Curiosity Receivable – Bonds").

-

Accrued Curiosity Payable: This account is usually discovered throughout the present liabilities part of the stability sheet. Much like receivables, sub-accounts can improve element (e.g., "Accrued Curiosity Payable – Financial institution Mortgage," "Accrued Curiosity Payable – Bonds Payable").

-

Curiosity Earnings: This account is discovered on the revenue assertion, reflecting the income generated from curiosity earned. It is essential to tell apart between accrued and acquired curiosity revenue. Accrued curiosity is acknowledged as revenue even when not but acquired.

-

Curiosity Expense: This account is discovered on the revenue assertion, reflecting the price of borrowing cash. Much like curiosity revenue, accrued curiosity expense is acknowledged even when not but paid.

Accounting for Accrued Curiosity:

The accounting entries for accrued curiosity are simple however require cautious calculation of the curiosity quantity. The overall journal entries are as follows:

Accrued Curiosity Receivable:

- Debit: Accrued Curiosity Receivable (will increase asset)

- Credit score: Curiosity Earnings (will increase income)

This entry displays the curiosity earned however not but acquired.

Accrued Curiosity Payable:

- Debit: Curiosity Expense (will increase expense)

- Credit score: Accrued Curiosity Payable (will increase legal responsibility)

This entry displays the curiosity expense incurred however not but paid.

Calculating Accrued Curiosity:

The calculation will depend on the rate of interest and the time interval. The essential system is:

Accrued Curiosity = Principal x Curiosity Price x Time

The place:

- Principal: The quantity of the mortgage or funding.

- Curiosity Price: The annual rate of interest.

- Time: The fraction of the yr the curiosity has accrued. That is normally expressed as a decimal (e.g., 3 months = 3/12 = 0.25).

Instance:

An organization has a $10,000 mortgage with a 6% annual rate of interest. The curiosity accrued for 3 months could be:

Accrued Curiosity = $10,000 x 0.06 x 0.25 = $150

This $150 could be recorded as an accrued curiosity payable.

Adjusting Entries:

On the finish of every accounting interval, adjusting entries are vital to acknowledge accrued curiosity. These entries make sure that the monetary statements precisely mirror the curiosity earned or incurred in the course of the interval. Failure to make these changes would result in misstated monetary outcomes.

Potential Pitfalls and Finest Practices:

-

Inconsistent Utility: Sustaining consistency in making use of the accrual technique is significant. Inconsistent utility can result in errors and inconsistencies in monetary reporting.

-

Incorrect Calculation: Errors in calculating accrued curiosity can considerably impression the accuracy of economic statements. Double-checking calculations is essential.

-

Lack of Documentation: Correct documentation of the curiosity calculations and the underlying agreements is important for audit functions and to make sure transparency.

-

Automated Methods: Using accounting software program with automated accrual options can considerably cut back the chance of errors and enhance effectivity.

-

Common Reconciliation: Recurrently reconciling the accrued curiosity accounts with financial institution statements and mortgage agreements helps establish discrepancies and stop materials misstatements.

-

Inner Controls: Implementing robust inside controls over the recording and processing of accrued curiosity transactions minimizes the chance of fraud and errors.

Affect on Monetary Statements:

Accrued curiosity considerably impacts the stability sheet and revenue assertion. Accrued curiosity receivable will increase present property, whereas accrued curiosity payable will increase present liabilities. Curiosity revenue will increase web revenue, whereas curiosity expense decreases web revenue. Correct recording of accrued curiosity is significant for a real and honest view of the corporate’s monetary place and efficiency.

Conclusion:

Accrued curiosity is a elementary facet of economic accounting. Understanding its nature, accounting therapy, and potential pitfalls is essential for correct monetary reporting and sound monetary administration. By implementing finest practices, comparable to common reconciliation, automated methods, and robust inside controls, firms can make sure the correct and well timed recognition of accrued curiosity, resulting in extra dependable and clear monetary statements. The cautious administration of accrued curiosity throughout the chart of accounts is not only a compliance requirement; it’s a cornerstone of efficient monetary stewardship. Ignoring it will possibly result in vital inaccuracies and probably severe penalties for the enterprise. Due to this fact, a deep understanding and constant utility of the ideas outlined above are paramount for any group.

Closure

Thus, we hope this text has supplied helpful insights into Understanding and Managing Accrued Curiosity within the Chart of Accounts. We thanks for taking the time to learn this text. See you in our subsequent article!