The Chart of Accounts: Spine of Monetary Reporting and Enterprise Administration

Associated Articles: The Chart of Accounts: Spine of Monetary Reporting and Enterprise Administration

Introduction

With enthusiasm, let’s navigate via the intriguing subject associated to The Chart of Accounts: Spine of Monetary Reporting and Enterprise Administration. Let’s weave attention-grabbing info and supply recent views to the readers.

Desk of Content material

The Chart of Accounts: Spine of Monetary Reporting and Enterprise Administration

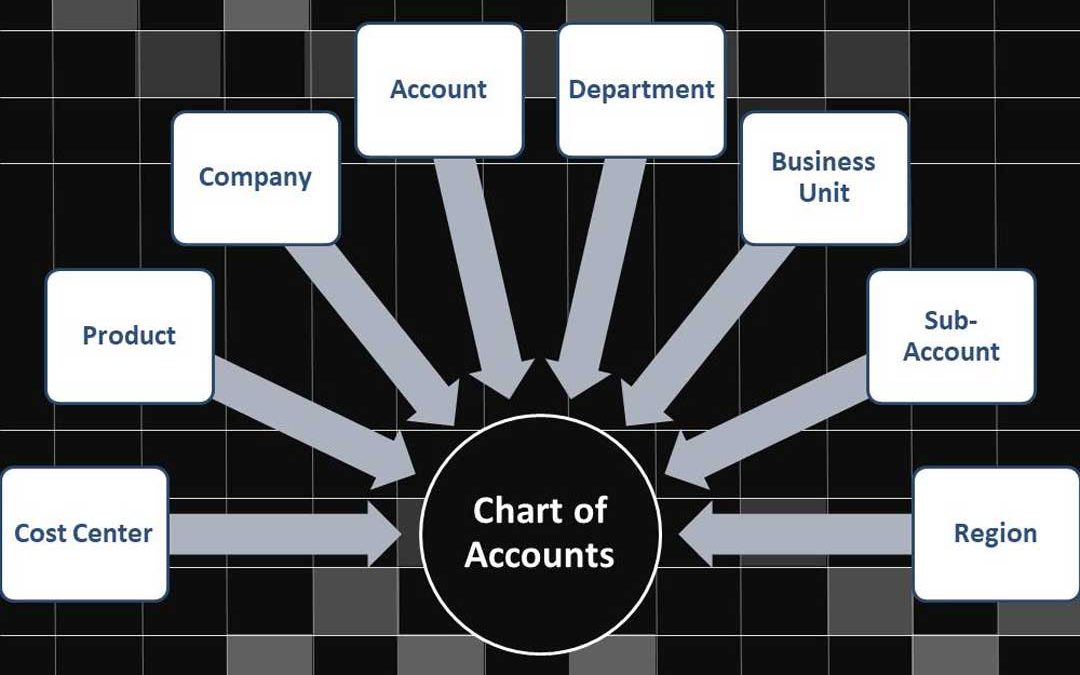

The chart of accounts (COA) is the bedrock of any group’s monetary system. It is a structured, organized record of all of the accounts a enterprise makes use of to report its monetary transactions. Consider it as an organization’s monetary dictionary, defining each account and its goal, permitting for constant and correct monitoring of revenue, bills, property, liabilities, and fairness. A well-designed and meticulously maintained COA is essential for correct monetary reporting, efficient administration decision-making, and compliance with accounting requirements. This text delves into the intricacies of the chart of accounts, exploring its construction, parts, advantages, and greatest practices for implementation and upkeep.

Construction and Parts of a Chart of Accounts:

A COA usually follows a hierarchical construction, organized by account kind and sub-accounts. The particular construction can fluctuate relying on the dimensions and complexity of the enterprise, trade, and accounting software program used. Nevertheless, the basic parts stay constant. These parts usually adhere to the essential accounting equation: Belongings = Liabilities + Fairness.

-

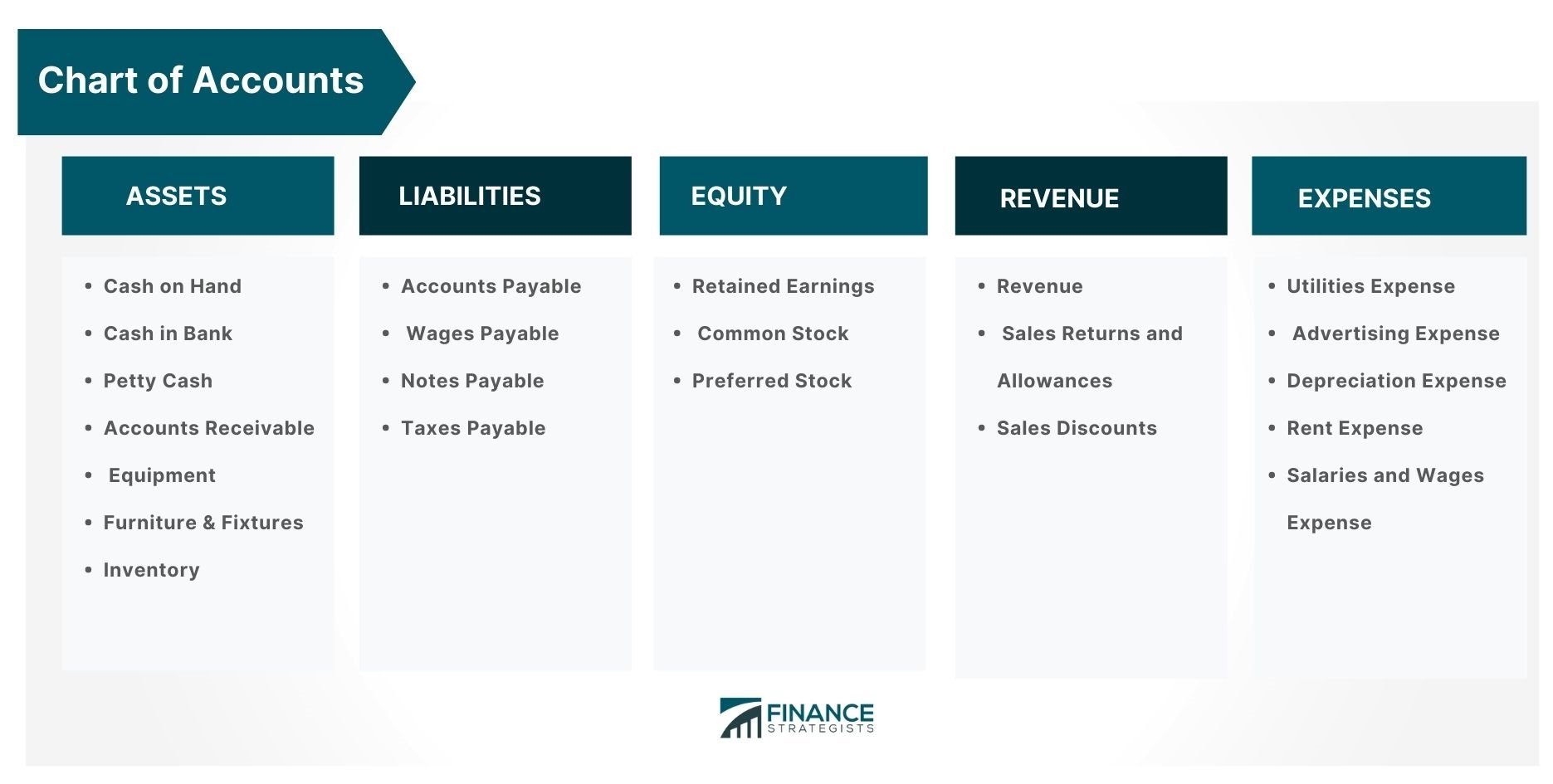

Belongings: These symbolize what an organization owns. The COA categorizes property into varied sub-accounts, together with:

- Present Belongings: Belongings anticipated to be transformed into money inside one 12 months, similar to money, accounts receivable, stock, and pay as you go bills.

- Non-Present Belongings: Belongings with a lifespan exceeding one 12 months, together with property, plant, and gear (PP&E), intangible property (patents, copyrights), and long-term investments.

-

Liabilities: These symbolize what an organization owes to others. The COA categorizes liabilities into:

- Present Liabilities: Money owed due inside one 12 months, similar to accounts payable, salaries payable, short-term loans, and accrued bills.

- Non-Present Liabilities: Lengthy-term money owed, similar to long-term loans, bonds payable, and deferred income.

-

Fairness: This represents the homeowners’ stake within the firm. For sole proprietorships and partnerships, it is likely to be merely known as "Proprietor’s Fairness." For firms, it contains:

- Widespread Inventory: Represents the funding made by shareholders.

- Retained Earnings: Collected earnings that haven’t been distributed as dividends.

-

Income Accounts: These accounts report revenue generated from the corporate’s main operations and different sources. Examples embody gross sales income, service income, curiosity revenue, and rental revenue. Income accounts are usually a part of the fairness part, as they enhance retained earnings.

-

Expense Accounts: These accounts observe the prices incurred in producing income. Examples embody price of products bought (COGS), salaries expense, hire expense, utilities expense, advertising expense, and depreciation expense. Bills cut back retained earnings.

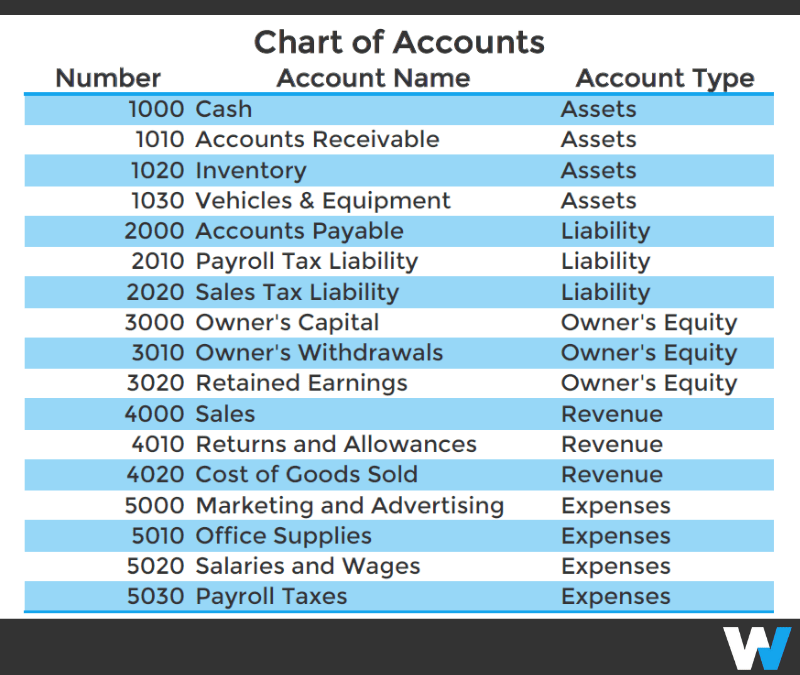

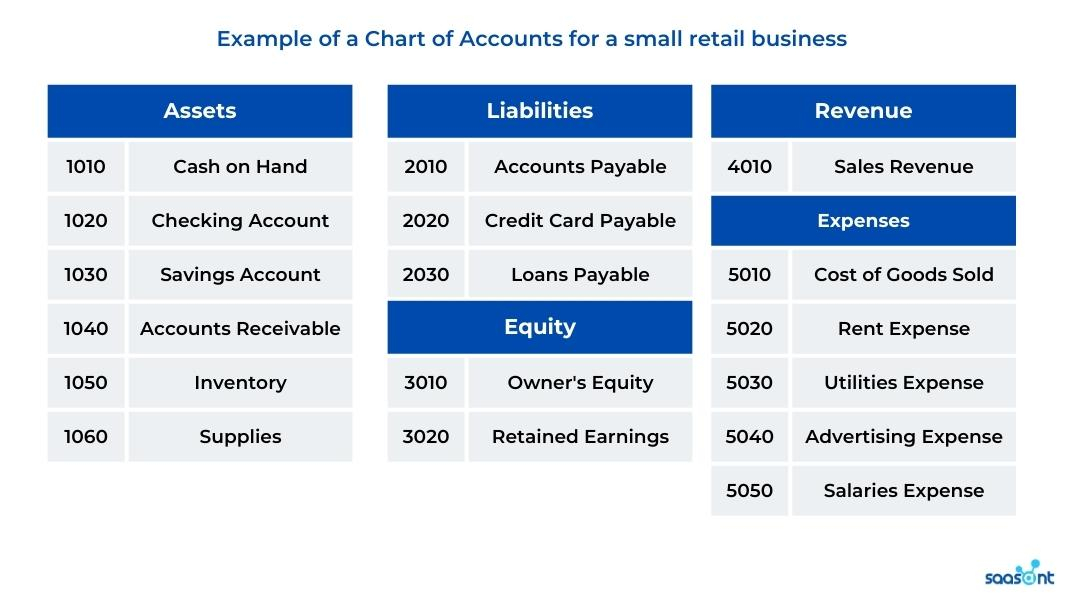

Numbering System and Account Codes:

A well-designed COA makes use of a constant numbering system to categorize and observe accounts effectively. This technique typically employs a hierarchical construction, with bigger numbers representing extra particular sub-accounts. For instance:

- 1000 – Belongings

- 1100 – Present Belongings

- 1110 – Money

- 1120 – Accounts Receivable

- 2000 – Liabilities

- 2100 – Present Liabilities

- 2110 – Accounts Payable

- 3000 – Fairness

- 4000 – Income

- 5000 – Bills

This structured numbering system makes it straightforward to find particular accounts, generate monetary studies, and analyze monetary knowledge. The extent of element within the numbering system will rely on the dimensions and complexity of the enterprise. A small enterprise could use an easier system, whereas a big company would require a extra detailed and complicated COA.

Advantages of a Effectively-Designed Chart of Accounts:

A well-structured and maintained COA gives quite a few advantages:

-

Correct Monetary Reporting: A correctly designed COA ensures correct and dependable monetary statements, offering a transparent image of the corporate’s monetary well being.

-

Improved Monetary Evaluation: The detailed categorization of accounts permits for in-depth monetary evaluation, enabling higher decision-making. Managers can observe key efficiency indicators (KPIs), establish developments, and assess the profitability of various enterprise segments.

-

Enhanced Budgeting and Forecasting: A COA facilitates the event of correct budgets and monetary forecasts, permitting for higher useful resource allocation and monetary planning.

-

Streamlined Auditing Course of: A well-organized COA simplifies the auditing course of, making it simpler for auditors to confirm the accuracy of monetary data.

-

Improved Inside Management: A correctly designed COA contributes to improved inside controls, lowering the chance of errors and fraud.

-

Compliance with Accounting Requirements: A well-designed COA ensures compliance with typically accepted accounting rules (GAAP) or Worldwide Monetary Reporting Requirements (IFRS), relying on the jurisdiction.

-

Higher Determination Making: The detailed info offered by a COA empowers managers to make knowledgeable choices relating to pricing, useful resource allocation, and strategic planning.

Greatest Practices for Implementing and Sustaining a Chart of Accounts:

-

Plan Rigorously: Earlier than implementing a COA, fastidiously take into account the corporate’s particular wants and trade greatest practices.

-

Use a Standardized Chart: Think about using a standardized chart of accounts as a place to begin, adapting it to suit the corporate’s distinctive necessities.

-

Maintain it Easy: Keep away from pointless complexity. The COA needs to be straightforward to know and use.

-

Common Evaluate and Updates: Recurrently overview and replace the COA to replicate modifications within the enterprise and trade practices.

-

Doc the COA: Preserve clear documentation of the COA, together with account descriptions and functions.

-

Use Accounting Software program: Make the most of accounting software program to handle the COA and automate monetary processes. This simplifies knowledge entry, reduces errors, and improves effectivity.

-

Prepare Staff: Present ample coaching to staff on the use and upkeep of the COA.

Conclusion:

The chart of accounts is excess of only a record of accounts; it is a essential device for managing and understanding a enterprise’s monetary efficiency. A well-designed and maintained COA is important for correct monetary reporting, efficient decision-making, and compliance with accounting requirements. By following greatest practices and repeatedly reviewing and updating the COA, companies can leverage this significant device to enhance their monetary administration and obtain their enterprise aims. Ignoring the significance of a well-structured COA can result in inaccurate monetary reporting, poor decision-making, and in the end, monetary instability. Due to this fact, investing time and assets in creating and sustaining a strong COA is a essential funding within the long-term well being and success of any group.

:max_bytes(150000):strip_icc()/chart-accounts.asp_final-438b76f8e6e444dd8f4cd8736b0baa6a.png)

![Ecommerce Accounting & Bookkeeping Guide To Best Practices [2024]](https://www.ecommerceceo.com/wp-content/uploads/2020/12/image-1024x598.png)

Closure

Thus, we hope this text has offered priceless insights into The Chart of Accounts: Spine of Monetary Reporting and Enterprise Administration. We hope you discover this text informative and helpful. See you in our subsequent article!