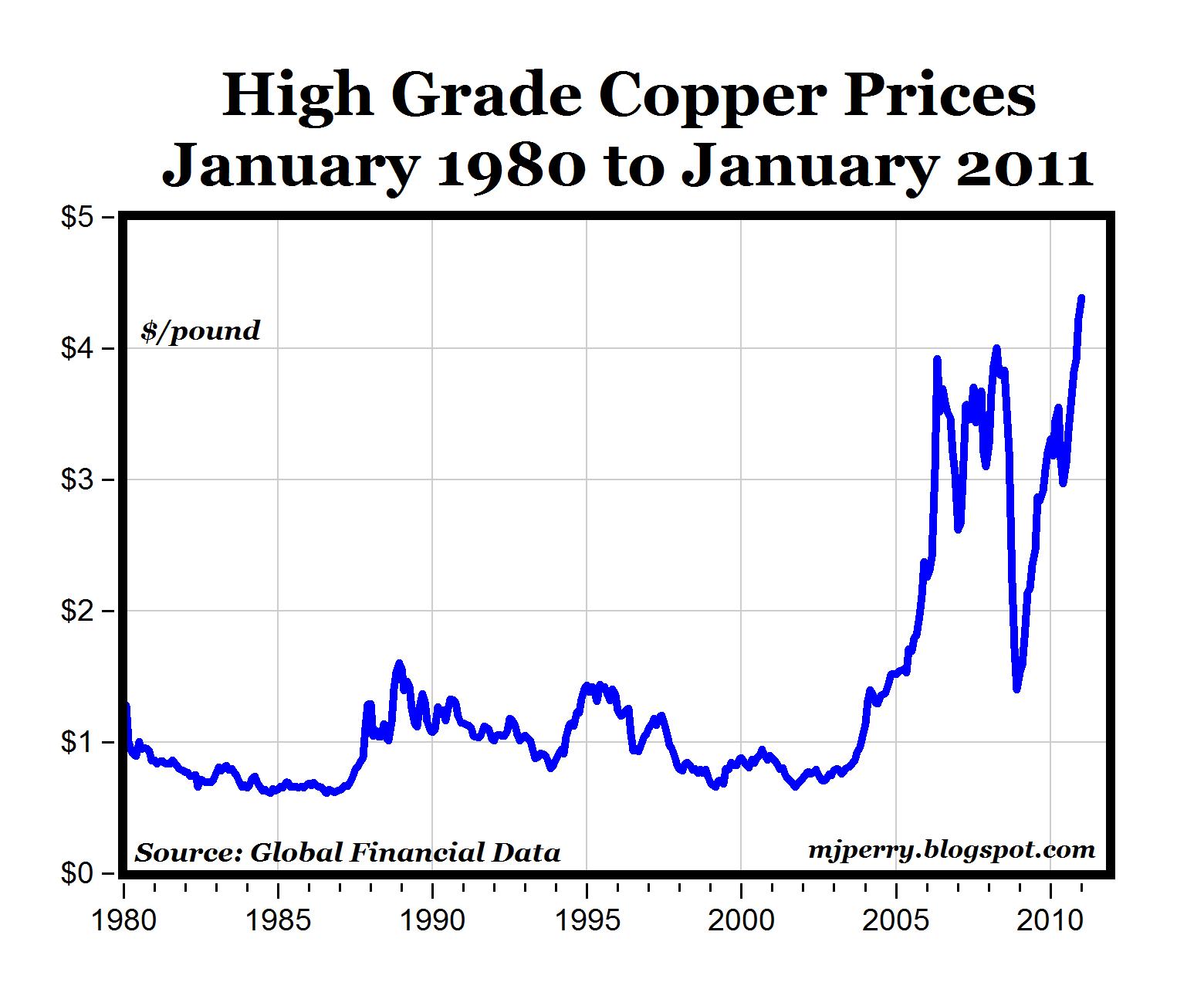

A Decade of Copper: Analyzing the Worth Chart from 2014 to 2024 (Hypothetical)

Associated Articles: A Decade of Copper: Analyzing the Worth Chart from 2014 to 2024 (Hypothetical)

Introduction

With enthusiasm, let’s navigate by means of the intriguing matter associated to A Decade of Copper: Analyzing the Worth Chart from 2014 to 2024 (Hypothetical). Let’s weave fascinating info and provide contemporary views to the readers.

Desk of Content material

A Decade of Copper: Analyzing the Worth Chart from 2014 to 2024 (Hypothetical)

The copper market, also known as a barometer of worldwide financial well being, displays an enchanting dynamic in its value fluctuations. Analyzing a ten-year value chart, say from 2014 to 2024 (utilizing hypothetical knowledge for the latter years), reveals a fancy interaction of macroeconomic components, supply-demand imbalances, and geopolitical occasions. Whereas a real 2024 chart is unavailable presently, we are able to assemble a believable state of affairs based mostly on present tendencies and skilled predictions as an instance the important thing components influencing copper costs.

2014-2016: A Interval of Decline and Volatility:

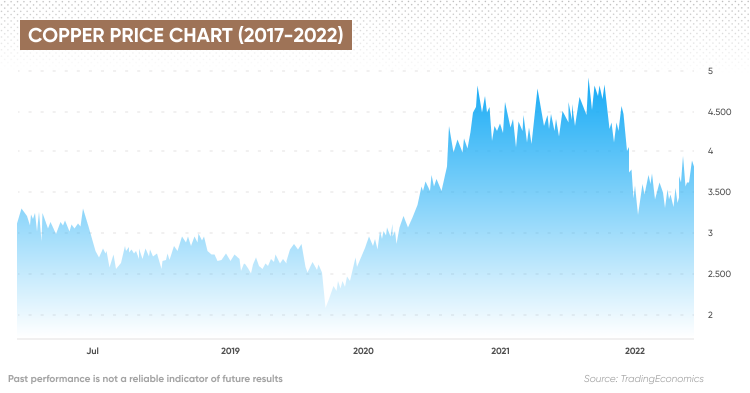

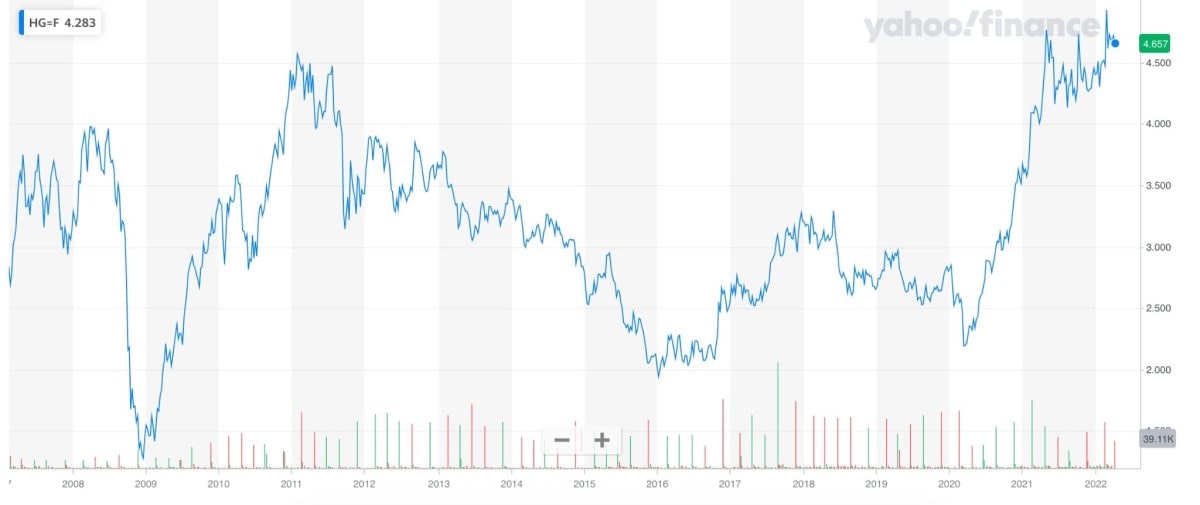

Our hypothetical chart begins in 2014, with copper costs hovering round $7,000 per metric ton. This era displays the slowdown of the Chinese language financial system, a significant client of copper. The decline, persevering with into 2015 and 2016, was exacerbated by oversupply from main producers like Chile and Peru. Elevated automation in mining additionally contributed to larger manufacturing volumes, additional pressuring costs. The value dip under $5,000 per ton in early 2016 marked a big low level, reflecting a pessimistic outlook on international progress and commodity demand. This era additionally noticed important volatility, with sharp value swings pushed by hypothesis and information associated to Chinese language financial insurance policies and international monetary markets. Geopolitical instability in sure mining areas additionally added to the uncertainty.

2017-2019: A Gradual Restoration:

A sluggish however regular restoration started in 2017, pushed by a number of components. Firstly, the Chinese language authorities carried out stimulus packages to spice up infrastructure spending, resulting in elevated demand for copper in building and manufacturing. Secondly, supply-side disruptions, akin to strikes in key mining areas, helped tighten the market. Thirdly, a weakening US greenback made dollar-denominated commodities like copper extra engaging to worldwide consumers. The value progressively climbed again in direction of $6,000 per ton by the tip of 2019, however remained unstable, reflecting ongoing considerations about international commerce wars and financial uncertainties.

2020-2022: The Pandemic and its Aftermath:

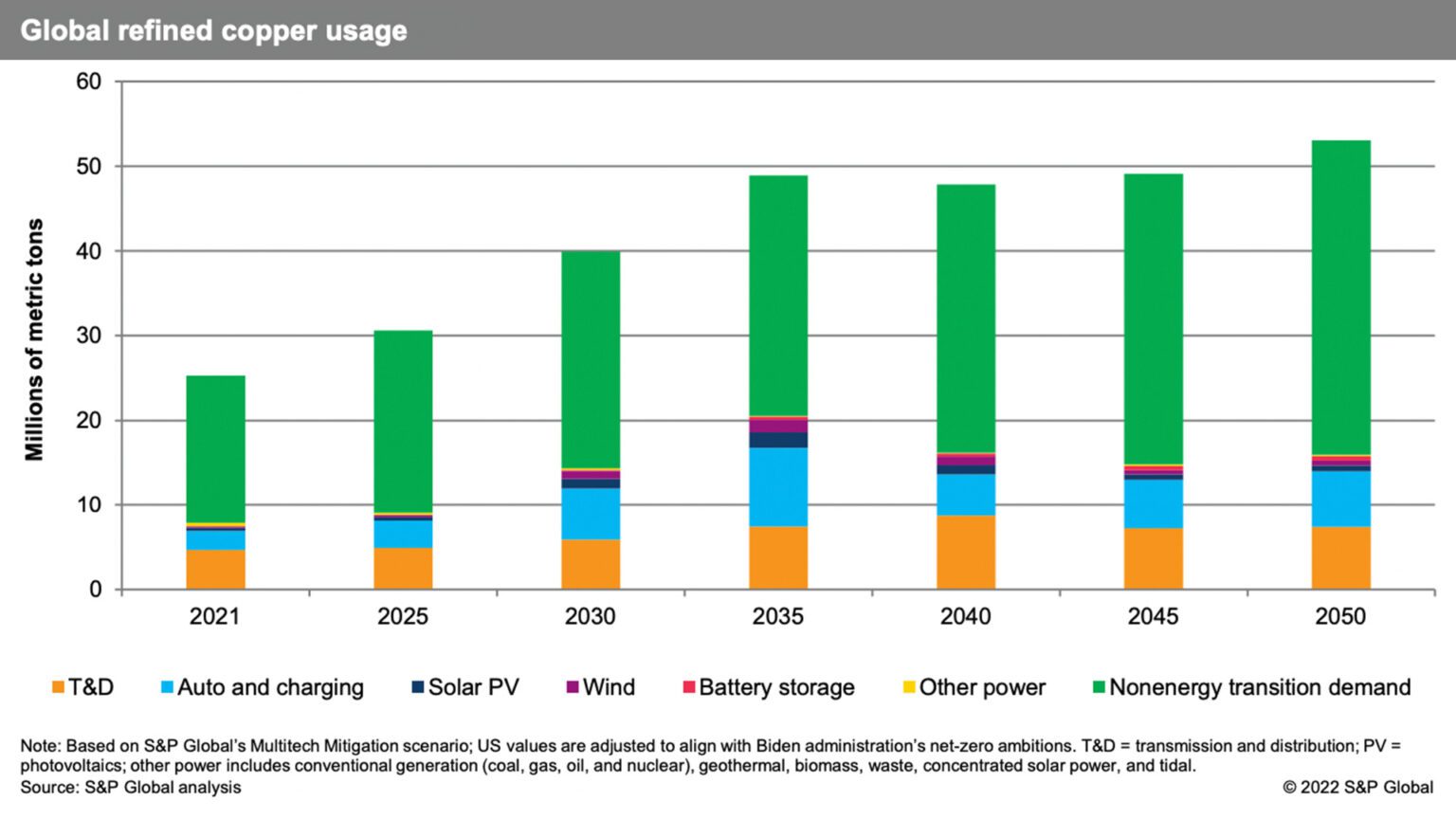

The COVID-19 pandemic in 2020 initially despatched shockwaves by means of the copper market, with costs plummeting as international demand contracted sharply. Nevertheless, the next unprecedented fiscal stimulus packages from governments worldwide, coupled with a speedy restoration in China, led to a exceptional rebound. The inexperienced power transition, with its heavy reliance on copper for electrical automobiles, renewable power infrastructure, and grid modernization, additionally began to considerably affect demand. Our hypothetical chart reveals costs surging past $8,000 per ton in 2021, pushed by this mix of things. Provide chain disruptions brought on by the pandemic additional contributed to cost will increase, as logistical bottlenecks constrained the move of copper to shoppers. The value remained elevated in 2022, albeit with some fluctuations reflecting considerations about inflation and potential rate of interest hikes.

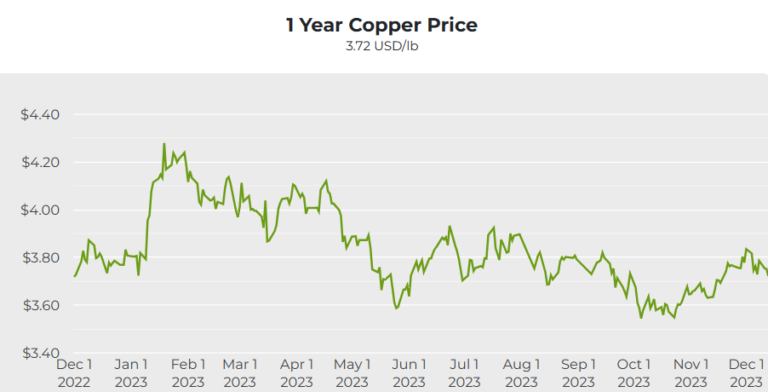

2023-2024: Navigating Inflation and Provide Constraints (Hypothetical):

Shifting into our hypothetical 2023-2024 interval, we see continued strain on costs. Whereas the inexperienced power transition continues to gas demand, inflationary pressures and rising rates of interest begin to influence general financial progress, probably dampening demand. Our hypothetical chart suggests a interval of consolidation round $7,500-$8,500 per ton in 2023, with some volatility pushed by financial knowledge and geopolitical developments. Provide-side constraints, together with the continued challenges in securing mining permits and the growing issue of extracting copper from lower-grade ores, proceed to play a big position. Nevertheless, elevated funding in new mining tasks and technological developments in extraction may probably alleviate a few of these constraints within the later a part of 2024, resulting in a slight softening of costs. The hypothetical chart may present a slight downward pattern in direction of the tip of 2024, however nonetheless remaining above the pre-pandemic ranges, reflecting the long-term structural shift in direction of a copper-intensive financial system.

Key Components Influencing the Hypothetical Chart:

A number of key components, past these already talked about, would contribute to the form of our hypothetical copper value chart:

- Chinese language Financial Development: China’s financial efficiency stays essential. Sturdy progress interprets to larger copper demand, whereas a slowdown can set off value declines.

- US Greenback Energy: A robust US greenback makes copper costlier for worldwide consumers, probably dampening demand.

- International Inflation and Curiosity Charges: Excessive inflation and rising rates of interest can sluggish financial progress, impacting demand for copper.

- Geopolitical Dangers: Political instability in main copper-producing nations or disruptions to international commerce routes could cause value spikes.

- Technological Developments: Improvements in mining expertise and the event of copper substitutes may influence provide and demand dynamics.

- Environmental Rules: Stricter environmental laws within the mining business may enhance manufacturing prices and probably restrict provide.

- Funding in Renewable Vitality: The continued progress of the renewable power sector will strongly affect copper demand within the coming years.

Conclusion:

The hypothetical ten-year copper value chart from 2014 to 2024 paints an image of a dynamic market influenced by a fancy interaction of macroeconomic components, geopolitical occasions, and technological developments. Whereas the specifics of future value actions stay unsure, the long-term outlook for copper seems optimistic, pushed by the rising demand from the inexperienced power transition and ongoing infrastructure growth globally. Nevertheless, navigating the challenges posed by inflation, provide constraints, and geopolitical dangers will probably be essential in figuring out the exact trajectory of copper costs within the years to come back. Cautious monitoring of those components, alongside steady evaluation of market tendencies, will probably be important for traders and companies working within the copper market. It’s very important to do not forget that it is a hypothetical state of affairs, and precise costs might deviate considerably relying on unexpected occasions and shifts within the international financial system.

.png)

Closure

Thus, we hope this text has offered priceless insights into A Decade of Copper: Analyzing the Worth Chart from 2014 to 2024 (Hypothetical). We thanks for taking the time to learn this text. See you in our subsequent article!